trying out something new

I'll keep this short and sweet, but I will be migrating my written posts about blockchain tech, venture investing, book reviews, independent research, and Placeholder blogs to https://www.gurnoornarula.com/.

beware of tokenizing everything

Chasing the goal of tokenizing every “real-world” asset relegates blockchains as secondary ledgers of truth rather than fulfilling their greater potential as the foundation for the future of internet finance. The attempt to tokenize everything is futile because we are in the business of developing net-new financial products that take advantage of being onchain rather than replicating existing assets. Furthermore, we should tokenize assets that supply some inherent value in being onchain - assets that actually have expressed demand from onchain investors.

In its current form, the tokenization space is primarily focused on treasuries, equities, commodities, and private credit. While these subsectors might experience some success with fringe retail investors onchain, I argue that we have already seen the strongest contenders for onchain tokenized success - stablecoins and tokenized treasuries.

Tokenization of U.S. Treasuries

There seem to be 3 fundamental inefficiencies in the traditional treasury market:

Settlement Delays: Advocates for tokenizing treasuries tout the benefits of instant settlement onchain, but I would argue that you forgo the benefits of multilateral netting. Maybe programmable settlement is a better term here. I’ve argue more about this in another piece.

Excessive Intermediation: This is ideally “solved” by being onchain, but I’m not sure this is true because current-day tokenization platforms are mostly nice frontends to represent the token, but the same messy backend filled with intermediary custodians, clearinghouses, etc. If anything, they add risk by introducing a centralized oracle network to report prices onchain.

Fragmented access to investment opportunities and a ;lack of consistent reporting.

While some of these issues may be resolved through tokenization, the real added risk is that of oracle risk, and we need to eliminate this risk by keeping everything onchain. This happens by either tightly integrating tokenized treasury products with onchian price feeds, or enabling thicker liquidity of these tokenized treasuries onchain.

We can then create a countercyclical hedge for DeFi because the inverse relationship between risk-free treasury yield rate and demand for stablecoins on-chain (cost of borrowing on-chain) - as risk-free rates rise, tokenized treasuries can absorb capital from pure stablecoins. when rates fall, capital flows back to DeFi lending and other onchain opportunities.

Tokenization of Equities

I understand the importance and demand of tokenizing U.S. treasuries as it provides risk-free yield in an otherwise volatile on-chain economy. However, I’m not sure what the demand for tokenized equities are, beyond just having it available on-chain. Given how yield-motivated the on-chain economy is, it seems like there are on-chain assets available with a similar risk profile as equities. Therefore, this implies that the demand for a tokenized equity for an onchain investor is close to zero.

This is further emphasized by the 10x principle: is purchasing a tokenized equity onchain 10x better for the end user than utilize an app on their phone or a trusted trading platform that they are familiar with? Not necessarily.

Tokenization of Commodities

Most folks view the tokenization of commodities markets optimistically because regulations don’t define commodities as securities, so they become inherently much easier to tokenize and trade on-chain. Furthermore, regulations emphasize custodianship and physical asset transparency, which plays well for tokenization. However, a major factor that is overlooked, yet obvious in hindsight, is that there is clear demand-side inertia in trading these commodity tokens on-chain. For retail crypto traders, they have shown limited interest in holding tokenized commodities, preferring Bitcoin as their store of value. For institutional players, they already dominate traditional commodities markets with access to sophisticated trading infrastructures and deep liquidity, so they don’t have a clear 10x reason to move to on-chain platforms.

The most popular on-chain commodity right now is gold, but there are markedly lower volumes and liquidity depths on digital exchanges. This under-performance can be credited to large price volatility and associated arbitrage onchain, which causes limited uptake on composable DeFi platforms like Uniswap or Morpho. Some of the more prominent issues these products have faced are:

Sudden dips in unchain liquidity or rapid premium fluctuations can trigger liquidations even when real-world gold price is stable

If an oracle price is used, custodian failures could allow attackers to purchase onchain gold at mis-priced levels

Instead of dealing with these issues that arise when catering to institutions who want physical asset settlement too, projects like Ostium are targeting purely synthetic commodity exposure that forgoe physical redemption. This approach is designed for margin retail traders, but experiences the pitfall of the actual demand for such an asset. They made capture short-term speculative demand, but it doesn’t seem like providing leveraged trading on commodity assets is a revolutionary financial product offering in an already volatile and high-yield on-chain economy.

Tokenization of Private Credit

Tokenized private credit has seen the most adoption behind stablecoins and U.S. treasuries, with large tokenized funds from BlockTower Capital, KKR, Hamilton Lane, etc. This is partially motivated by the plethora of issues that private credit markets face with illiquid secondary markets, inefficient price discovery until maturity, and limited access to investment opportunities. These issues frame tokenization of private credit as a silver-bullet solution, but the major roadblock here is strict regulation surrounding private credit.

Projects that tokenize private credit quickly face issues of being termed as being investment companies or offering securities in the form of tokens. This is broken down further below as there are two main approaches of tokenizing private credit in the market today:

Loan-Specific Tokens: Each private credit loan is tokenized to represent an investor’s claim on the asset’s underlying cash flow. The issue with this approach is that these tokens can constitute securities and must be offered under exemptions. While possible to implement on-chain, this raises the question of why someone would want to conduct said transaction onchain if they face the same, if not harder, hurdles to purchase the asset - they might as well do it off chain with more established trading infrastructure.

Lending Pool Model: Lenders contribute liquidity to a general managed lending pool, and Pool Delegates allocate loans to borrowers. These Pool Delegates are usually KYC’d specialized banks or institutions. The issue here is that pool tokens form a lending pool may constitute an investment company.

I think the major upside here is for institutions who want to leverage onchain rails on the backend to decrease their operational and management costs of private credit financial products. Therefore, the big winners here will be infrastructure companies providing these services, and these institutions are responsible for providing these tokenized financial products to their investors with minimal additional overhead to the investors to make said investment. If there is additional user friction, staying off chain is just easier.

This gap between the onchain and offchain economy will continue to exist until a blockchain is recognized as a regulated source of truth. Until then, this distinction creates two distinct financial systems. I strongly believe that we should utilize the tools at our disposal to create net-new financial products that advance the internet economy rather than tokenizing “real-world” assets that relegate blockchains as secondary sources of truth.

T + x.xxx (Programmable) Settlement

Financial institutions continue to explore decentralized systems for securities settlement and clearing with heightened interest given the touted benefits: instant settlement, the (theoretical) elimination of all counterparty default risk, and the subsequent elimination of the need to post expensive and unproductive collateral. But is porting our financial clearing and settlement infrastructure on-chain the holy grail solution? While our current system is plagued with inefficiencies, radically shifting to instant settlement models is a regression. Instead, we should explore the common middle ground of precise settlement, taking advantage of programmable decentralized infrastructure to remove ‘arbitrariness’ from our current system while drawing on benefits from both sides of the spectrum.

On one side of our settlement spectrum is Central Clearing Party (CCP)-based multilateral clearing and settlement, which revolves around T+c (c denotes some constant {1, 2, 3}) settlement. This delayed settlement time serves as a date of finality, allowing the counterparty to obtain said promised asset to transfer up to c days after the agreement of some trade. In this environment, (1) centralized clearinghouses can perform multilateral netting, thereby resolving accounts payable from accounts receivable with greater transaction efficiency, (2) investors exercise the opportunity to borrow against proofs of purchased assets, and in general, (3) we establish a trusted third-party to reduce counterparty risk while extending credit and margin.

On the other side of the spectrum, we have the proposed T+0, or instant, settlement. In this model, we transition from a market-wide settlement system to a transaction-by-transaction model. The instant settlement model (theoretically) improves the expressed shortcomings of the CCP-based model. It bilaterally settles each transaction between two parties that are (theoretically) not exposed to counterparty risk as settlement is programmed and completed synchronously with the trade agreement. Moreover, this (theoretically) circumvents the need for centralized third parties and unproductive collateral, as the source of counterparty reputation is guaranteed by programmable atomic settlement compared to staked funds.

Note the repeated use of ‘theoretically’, hinting at the fact that while this solution in all cases may sound like the desired end product, it has some critical implementation flaws.

The key value of CCPs interposing themselves as middlemen is to perform multilateral netting and decrease counterparty risk as a trusted anchor and trading partner. The key value in instant settlement is the elimination of involved financial risks, middlemen, and unproductive capital. In the spirit of balance, we meet in the middle with a proposed solution: precise settlement.

I extend to define precise settlement as T + x.xxx settlement, an opportunity for counterparties to perform programmable trades with optimal levels of staked collateral while permitting contract-enabled ‘CCPs’ to conduct multilateral netting.

For example, instead of institutional trading partners locking into a T+2 settlement contract (common for equity trades) with a generic amount of staked collateral, they can agree to a programmable T + 1.2 settlement contract (1.2 ~ 1 day and 5 hours, and this value can be further broken down into detailed time intervals) and utilize a precise calculation for the optimal collateral level to be staked.

How does this meet in the middle of the spectrum, combining strengths from both extreme models?

Continuing under the premise of our example, we can highlight a multitude of strengths

Precise asset delivery: The institutional trading partner responsible for delivering the asset knows exactly when they need to have the asset in possession, and the recipient knows exactly when they will receive the asset or a default payout. This is a step forward from the otherwise arbitrary trade agreements signed by CCP-based settlement contracts.

Multilateral Netting: We retain the ability for our contract-based ‘CCP’ to perform multilateral netting instead of reverting to inefficient processes of bilateral, transaction-per-transaction trade netting.

Proof of Purchased Assets: We also retain the ability for trade partners to utilize their Proof of Purchased Assets as assets within the secondary market as the precise time delay allows for the continuous use of promised assets, albeit not executed yet.

Optimal staked collateral: Arbitrary contract terms = Arbitrary staked collateral amounts. Precise settlement models allow us to potentially derive optimal levels of collateral based on the selected time delays on the settlement contract, allowing for trade partners (especially smaller players) to effectively conduct trades without having to stake unproductive and expensive capital.

With reinvigorated interest in the space, many components are slowly coming together to make this possible. There is advancing research on compliant blockchain networks and permissioned token standards which is vital to building a programmable on-chain ‘CCP’. Efficient smart contract development will help unlock the concept of programmable and precise settlement contracts. We can also play with newer forms of decentralized on-chain identity, thereby establishing institutional trust anchors and recognized trade partners.

One concept that warrants research is optimal collateral levels. Thus far, collateral levels are determined by margin levels in the default pools of the CCP as well as the average position of the trade partners in the open market. However, these are frequently too expensive for smaller trade partners, leading to an unfavorable ‘no competition’ environment and arbitrary amounts of unproductive collateral. However, by deriving a model for optimal collateral levels as a function of the time delay x.xxx as well as other factors, we can ensure a competitive trading environment while only staking the amount that needs to be staked.

It has become abundantly clear that decentralized crypto-networks are potential solutions to some existing inefficiencies, such as the current settlement and clearing system. That said, a complete overhaul, represented by moving from one end of the spectrum (CCP-based settlement) to the other extreme (instant settlement) is a step backward. However, I believe that meeting in the middle combines the best of both worlds.

Wallet-Centrism

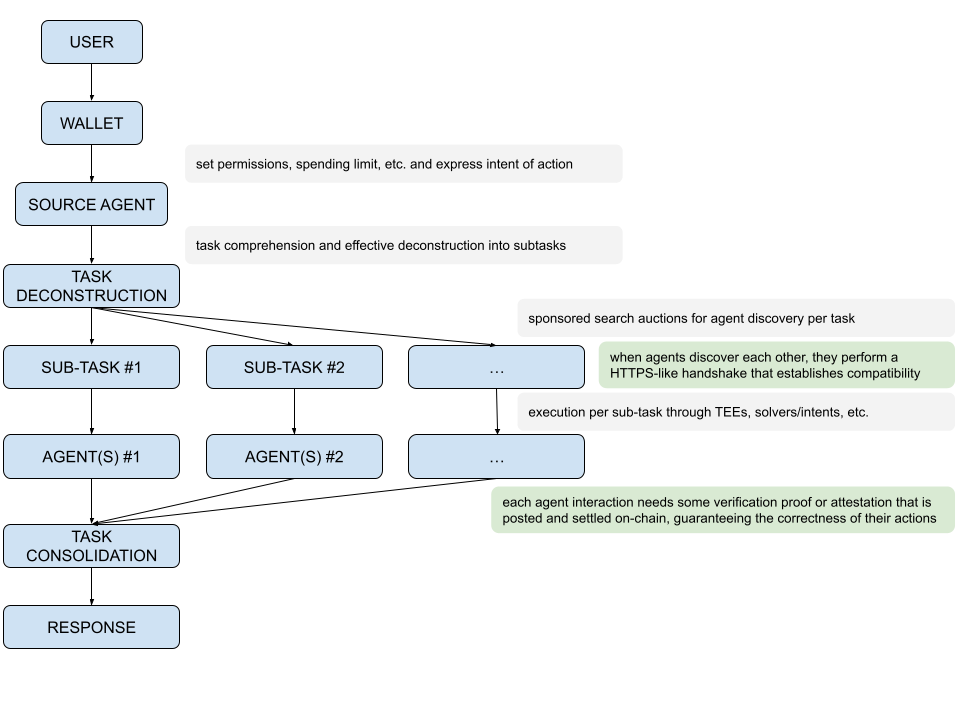

We are transitioning to an environment where users want to outsource and automate time-consuming yet complex tasks. Lower attention spans create opportunities for personalized autonomous agents that humans can utilize to delegate task execution. We've seen this already, where users have begun to transition away from numerous distinct websites and search queries for data in favor of text-prompted LLMs that provide a universal set of answers in one terminal. The natural next step is a locally-hosted autonomous agent that is trained on all your personal data - an autonomous extension of you.

In this future, these powerful first-point operator agents will need to receive, understand, process, and respond to complex user requests. To do so effectively, they will be in charge of breaking said task into easier-to-complete subtasks. For each of these subtasks, the operator agent will be in charge of discovering, contracting, and coordinating a set of purpose-specific agents aka finding allocative efficiency.

How do we ensure that you can securely delegate your identity to an autonomous agent, while also making sure there is a universal destination for your off-chain and on-chain identity (permissions, authentication, passkeys, public/private keys, digital signatures, etc.)?

It is my current belief that this universal destination for an “autonomous extension of you” is a self-custody on-chain wallet. Wallets become a source of your cryptographically-secure digital identity that can generate attestations for off-chain and/or on-chain agentic interactions on your behalf.

The graphic above showcases user flow for their intents rooted in this wallet-centric belief. Regardless of what form factor the wallet itself will take (desktop plug-in, mobile application, chatbot interface, speech-to-text, etc.), a user will interact with their wallet as a destination for any action: on-chain or off-chain. And they can do so because their universal set of authentication permissions no exist in a self-custody manner rather than being provided by some centralized web2 OAuth 2.0 provider.

Our lives are becoming more digital and having a fragmented identity controlled by centralized authentication providers seems outdated. Utilizing a cryptographically-secure extension of your digital extension that bridges the on-chain and off-chain worlds is a pressing need.

flexible programmable sequencing

Much of this piece is inspired by and, in part, a reflection of "SoK: Cross-Domain MEV" by Conor McMenamin.

There is an obvious rise of shared sequencers, settlement layers, and superbuilders. This shift has brought the concept of cross-chain extractable value to the forefront, challenging us to quantify and mitigate its impact across multiple domains. I wanted to utilize this piece to document and discuss some key learning from Conor’s piece, “SoK: Cross-Domain MEV”.

One of the most pressing issues in this space is time-dependent extractable value. The naive solution of simply decreasing block confirmation times comes with its own set of challenges. Increasing base chain throughput risks centralization, while fast inclusion confirmations on slower chains face technical hurdles. However, the idea of a decentralized shared sequencer network (see Astria) with immediate soft commitments and atomic cross-chain transactions is pretty interesting. Under ideal conditions such as immediate soft commitments (Astria clock in at ~1 second) as well as atomic cross-chain transactions, the system could potentially mitigate much of the signal and time-dependent extractable value we currently grapple with.

Yet, there are a couple of persistent questions to address. How do we ensure that pre-sequenced bundles from various rollups are built in the correct order? What's the best approach for validating cross-dependent transactions across multiple rollups? The need for verifiable builders and accurate sequencing of cross-rollup transactions adds another layer of complexity to an already intricate system.

Interestingly, the introduction of programmable intents with embedded cross-chain dependencies might level the playing field between single-domain and shared sequencers. Meanwhile, app-chains offer a promising solution to the state staleness problem, potentially providing a superior experience for certain applications. However, they come with their own cross-chain limitations.

Another interesting point was slot auctions for builders. The idea of a secondary market for building rights presents both opportunities and challenges. While it could help distribute centralization risks, the already oligopolistic nature of cross-domain building raises concerns about creating new single points of failure.

It’ll be interesting to see the quantification of cross-chain extractable value as we develop shared interoperable domains. However, the line continues to blur, and I think we will soon see flexible domains of verifiable and programmable sequencing rules. This’ll enable everything from application-specific ordering rules for priority interaction to based rollups with fast confirmation and asynchronous composability.

The views and opinions expressed on this article are solely those of the original author and mentioned contributors. These views and opinions do not necessarily represent those of Placeholder Management LLC or its team.

ai agents as animated memecoins

Memetic frenzies seem to dominate the early adoption of any technology in this sector. And given a blockchain’s openness, each of these frenzies are usually attributed with a financial token that showcases their relative social value. It manifested early with memecoins tokenizing real-world events, internet memes, and other cultural trends. Now, early versions of AI agents represent an extension of memecoins as they have live capabilities and are also financialized for community involvement.

Most of these early agentic platforms closely represent memecoins with live extensions such as creative content creation, real-time streaming, or even financial alpha. These are naive first steps that showcase increasingly blurred lines between agents and humans for basic tasks. What makes them unique, however, is that we’ve paired freebased AI agents with creative inputs/outputs, and financial independence through self-hosted wallets and associated tokenization. Now, not only can individuals speculate on stagnant memes, but can have financial skin-in-the-game for dynamic agents that not only represent memetic culture, but also produce content and engage with their community.

But when do we move on from early memetic experiments and onto more practical use cases?

The transition from early memetic experiments to practical use cases in the realm of AI agents is already underway, with significant advancements emerging in integrated agentic ecosystems on platforms like Base and Solana. These ecosystems are paving the way for sophisticated agent-to-agent interactions, marking a shift towards more tangible applications. Two key developments stand out: hyper-personalized agents and secure autonomous on-chain trading with robust risk management protocols. A prime example of this evolution is Coinbase's initiative to create fully-autonomous DeFi management agents within their wallet ecosystem. This innovative approach allows users to delegate their funds to personalized agents capable of making informed investment decisions based on user-defined parameters such as preferred assets and risk tolerance. Such practical applications demonstrate that we are moving beyond the initial experimental phase, and into a fully on-chain agentic environment.

The views and opinions expressed on this article are solely those of the original author and mentioned contributors. These views and opinions do not necessarily represent those of Placeholder Management LLC or its team.

let's build something people can use

Thanks to the Placeholder investment team and Tim Robinson for the discussions here, our conversations inspired some of these takeaways.

Programmable and verifiable on-chain actions should make applications easier, more intuitive, and safer to use for consumers since they remove any ambiguity that is associated with human middlemen. However, we consistently see the opposite result, as is evident by how infrastructure-heavy the industry is. The reason web3 is harder, less intuitive, and perceived as a risky platform to use is because we build from an infrastructure-first mindset and are yet to implement basic design principles that provide users with the confidence to utilize web3-native applications.

Normie users’ gateway to interact on-chain needs to have minimal touchpoints to get started. In the current state, most competitive wallet services require 7+ complicated touchpoints until a user can even begin performing on-chain financial actions. It’s hard enough to understand what “transacting on-chain” actually means, and introducing complicated steps such as saving seed phrases or on-ramping fiat with awfully high fees doesn’t make this journey any easier. Furthermore, on-chain identity remains an unresolved issue, but a long string of characters secured by a private key and seed phrase is certainly not a user-friendly solution. Until an elegant solution for integrating an individual’s web2 identity on-chain can be pioneered, innovative wallet teams such as Sui and Aptos are working on zk-enabled or keyless wallet log-in schemes, respectively, allowing users to retain their familiar web2 internet accounts while transacting on-chain.

The leap to begin interacting on-chain is massive because of a lack of familiarity with the technology. Let’s not make it harder by introducing complex terminology and features. Let’s also not accept these design standards as acceptable because a deeply-motivated crypto-maximalist is willing to overlook these obvious hurdles. We’re building for everyone, not an interested few.

Another pressing area of concern is the incredibly high learning curve and lack of security features that users encounter, leading to a lack of confidence when using web3 wallets. In web2 financial environments, basic tools that help walk the user through an application or fundamental features such as insurance give a new user confidence and help the user establish trust in the service. However, web3 applications assume a crypto-native user, leaving normie users with virtually no options to onboard onto these apps. Innovative implementations of chain abstraction coupled with principles such as intuitive walk-through features within an app and insurance for interacting with risky chains will take us a long way in designing intuitive web3 gateways for normie users.

The applications vs. infrastructure debate is one of the most redundant in the industry, but if we do feel that infrastructure is at a point where we can support a new class of applications, let’s ensure we are building with a user- and design-first approach.

The views and opinions expressed on this article are solely those of the original author and mentioned contributors. These views and opinions do not necessarily represent those of Placeholder Management LLC or its team.

is privacy a commodity?

Thanks for the discussions Mario and Aadharsh, our conversations inspired some of these takeaways.

There’s an interesting tug-of-war at play with privacy-first projects and optionally-private incumbents. By principle, blockchain infrastructure is designed to be public, but the limitations of this design principle when deploying applications has become glaring obvious. Hence, the reason for implementing privacy-enhancing technologies within the blockchain stack.

On one side of this tug-of-war, you have privacy purists who are implementing alternatives to pre-existing infrastructure and applications, but with privacy technology in-built. These players are exemplifying core Internet security design principles, as stated in my CS textbook from college:

“Trying to retrofit security to an existing application after it has already been spec’ed, designed, and implemented is usually a very difficult proposition. Backwards compatibility is often particularly painful, because you can be stuck with supporting the worst insecurities of all previous versions of the software.” - UC Berkeley CS161

The other side acknowledges the network effects at play with incumbent blockchain infrastructure solutions and is approaching privacy as an important plug-and-play feature to exist on top of the existing stack. This is effectively treating privacy as a commodity.

While I acknowledge the strength of the first argument and the importance of privacy as an in-built design feature, recent advancements have demonstrated the validity of the second approach as well.

For example, going “full ZK” has become easier with Optimistic rollups gaining the ability to implement this PET. I recall not long ago when folks regarded the OP stack as a dead model given the eventual proliferation of native ZK rollups. We’re also seeing modular execution networks layer on top of existing VMs, equipping developers with confidential compute and privacy features without leaving their native development language or familiar execution environment.

Current infrastructure and application products are relatively popular without having privacy as a get-go feature. They’ve reached a certain scale of network effects. While they may be de-throned, it seems an upward battle to compete with incumbents on the principle of privacy. Like it or not, privacy may be an important add-on feature, but people seem to be comfortable with alternative solutions that offer better user experience or have reached a sufficient scale.

The views and opinions expressed on this article are solely those of the original author and mentioned contributors. These views and opinions do not necessarily represent those of Placeholder Management LLC or its team.

marginal improvements aren't enough

Thanks for the context and discussion Brad, our conversation inspired some of these takeaways.

By definition, DePIN is any coordination network that creates a buyer and seller market for some type of data. By that argument, a Layer 1 blockchain like Ethereum can be framed the same way, where sellers provide digital assets and on-chain services to buyers, who utilize this infrastructure and ETH to pay for these transactions. In this vein, the reason Ethereum has been incredibly successful is because it provides a 10x upgrade to existing methods of transacting and storing state: it does so in a transparent, programmable, and trustless way.

What most DePIN projects fail to identify is that to obtain a majority of an existing market, their offering has to be 10x better than the competition. They can’t rely on a marginally-better set of data that is collected in a permissionless, decentralized, and transparent manner because, frankly, buyers do not care as long as the data is somewhat reliable. And in most existing data markets, it is. The question DePIN projects need to ask is how to increase the quality, reliability, frequency, diversity, etc. of the data they are collecting and selling, which can absolutely be achieved through a blockchain backend.

Another approach is to utilize DePIN to empower individual data providers that are otherwise censored or unable to contribute data to a global network. This questions the relationship between individual <> state. With data that is more sensitive, is actively censored, or is not actively monitored by the state, is it possible that individual citizens could override some state restrictions or shortcomings to provide visibility into this data with Internet-connected devices? This intersection could be an exciting area of opportunity for DePIN projects where independent coordination networks could provide a more accurate and holistic view while providing a resolution to state <> individual tensions.

It has become increasingly obvious that principles of privacy, transparency, and decentralization tacked on to a marginally better product is not enough. While most DePIN networks fall victim to this quality, there exist exciting areas of innovation where DePIN projects can provide strictly better data than their centralized counterparts or shed light to new data sources that are otherwise restricted or unavailable by empowering individual citizens.

memecoins are the first crypto-native video game

We had a very interesting team research meeting last week centered on intellectualizing memecoins. We could very well be overthinking this framework, and in reality, memecoins exist as a 24/7 global casino, but it's an interesting exercise nevertheless.

We were debating the extent to which memecoins actually represent something - a cultural artifact, a real-time event, a digital meme, etc. While some of us concluded that memecoins serve as a way for people to hold stake in an artifact they align themselves with, Joel brought up an interesting analogy that I agree with - memecoins are the first successful crypto-native on-chain video game.

The core components of any game are goals, rules, challenges, and interactivity. Memecoins can then act as a 24/7 global game played on a multitude of platforms (exchanges and wallets) with these same principles. The goal for any player is to maximize their portfolio balance, and the value of their portfolio provides real-time updates of their performance. The rules of the game are simple: maximize your portfolio by trading a variety of available assets at profitable positions. Traders can develop interesting chart-reading strategies by combining off-chain social and on-chain price movement indicators. The challenges are the volatility of an asset’s performance and the timing of a profitable trade. As for interactivity, the blend of social influence and momentum-driven investing is arguably the most interactive way to engage with such a game.

The reason I agree with this framework more so than the counter is because I loosely believe that memecoins don’t represent something inherently valuable. The conversion rate of people that believe or align themselves with something to those that place financial stake in that thing seems very low. Most memecoins are manifestations of digital memes or real-world events, and a certain set of people may care deeply about these artifacts. However, I believe a majority don’t care enough to place financial value in a representative and volatile token simply to align themselves with that artifact.

While it will remain an interesting space to track and certainly one that isn’t going away, I think it's important not to overvalue a phenomenon that may just be an entertaining, speculative, and successful game that happens to be crypto-native.